Early projections on steel markets in the United States predicted that the construction industry might see fluctuations, but that overall, the industry wouldn’t be hurt by fluctuating prices. And then COVID-19 swept the world. Now, the picture looks quite a bit different. One factor is that China, where the virus started, is the world’s largest steel producer. They process and refine 97% of the manganese used in steel production along with silicon and other important raw materials. January saw a sharp spike in the costs of these materials as COVID-19 slowed manufacturing in China.

So now that we’re in the age of COVID-19, what’s in store for the steel industry? Let’s take a look at recent data to find out.

Chinese Production Slowdown

Since China is such a major player in the global steel industry, this is a big indicator in how the U.S. steel industry will fare. Data from the American Metal Market shows that the week of February 6, steel inventory began to accumulate within China. This was because steel mills were slowing or stopping work on account of COVID-19, which left them unable to produce products and deliver them to end users. Transportation companies also struggled to bring finished products to port.

This led to forecasts that demand for steel would lessen within the first quarter of 2020 as sectors like construction, building and machinery manufacturing experienced slowdowns in response to the virus. Those forecasts proved partially correct: In the United States, steel production dropped 12.7% year-over-year as of March 28.

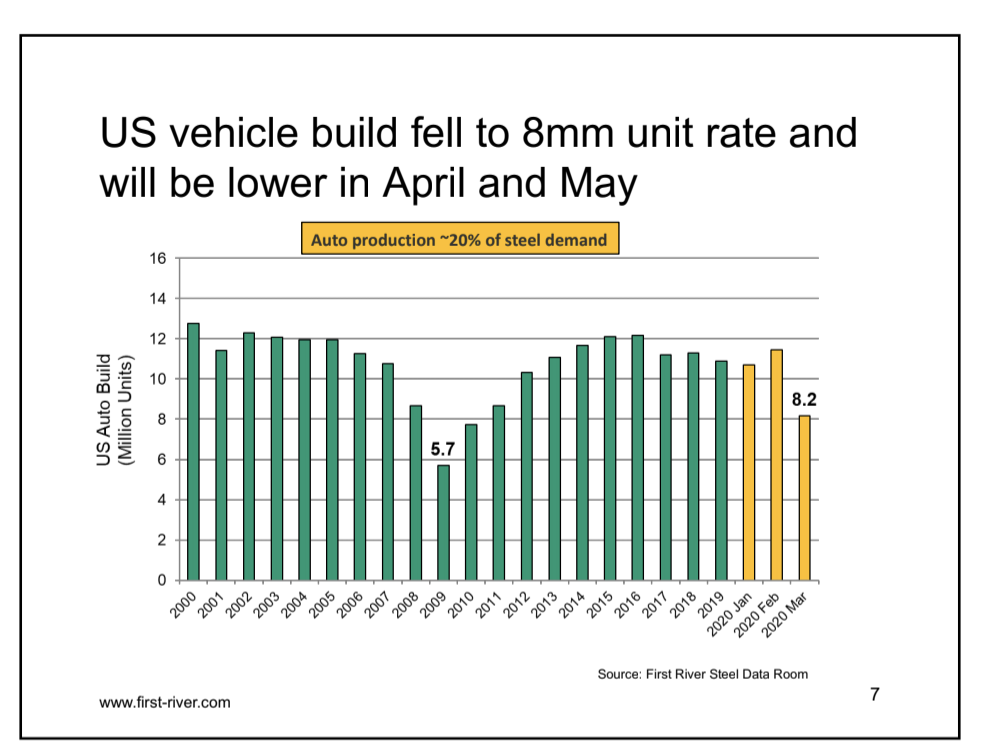

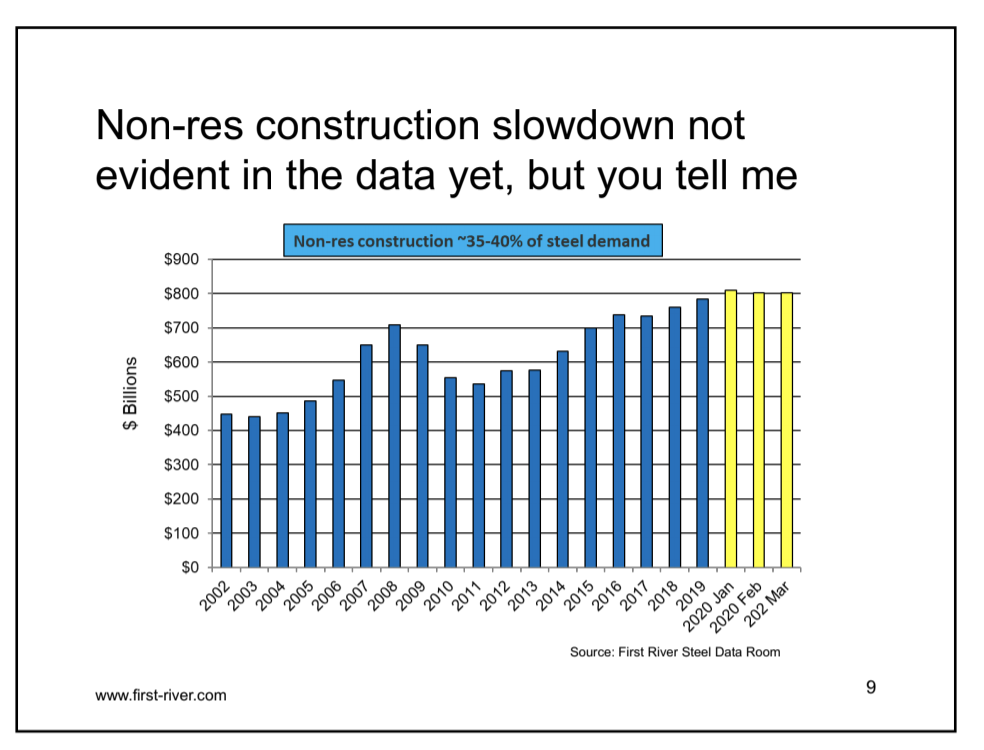

Which steel sectors are hardest hit? Auto manufacturing has seen a sharp downturn, with data revealing a sharp drop in the millions of units produced. Housing starts have dropped slightly, and oil rig counts are down, but non-residential construction remains strong.

What Does the Future Hold?

There’s still so much uncertainty that it’s impossible to predict quite what the impacts of COVID-19 on the U.S. steel industry will be. However, events like the 2009 financial crisis provide some insights as to how things could go—though bear in mind that the crisis stemming from the pandemic is unlike any other financial crisis for a variety of reasons. In this case, while history may provide insights, it is not the most accurate in predicting the future.

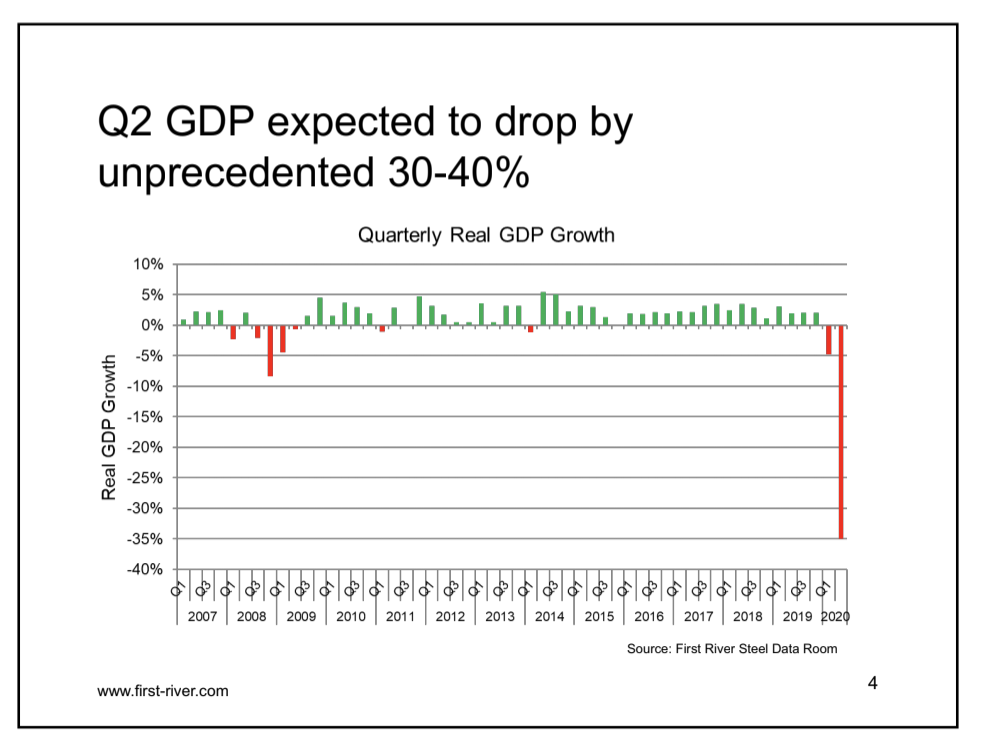

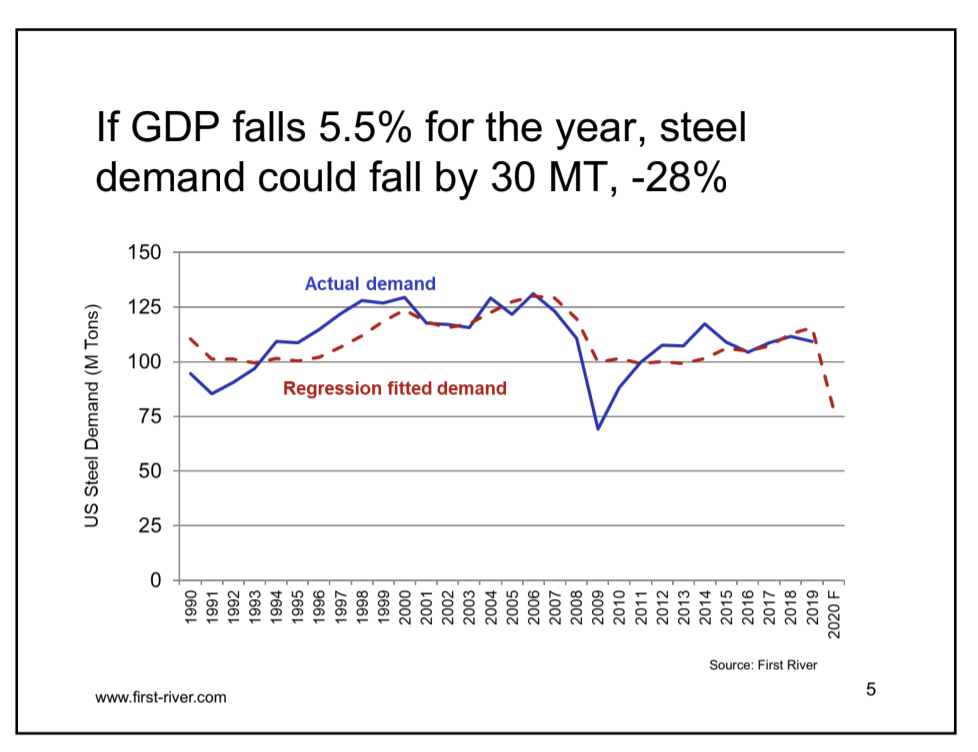

With that in mind, data on the 2009 financial crisis shows that gross domestic product within the U.S. fell by 2.5%. Along with the GDP decline, demand for steel fell 37%. Economists are forecasting a 30% to 40% drop in GDP in the second quarter of 2020 on account of COVID-19. Data shows that a 5.5% drop in GDP could signal a 28% fall in steel demand, so it’s within reasonable assumptions that if the GDP falls further, steel demand could tumble.

Much Rests on the Automotive Industry

Demand is the biggest factor that will determine how quickly and how well the steel industry recovers. Right now, demand is down largely because the automotive industry has slowed production. Among the automotive industry, there are several major issues causing the disruption to production. Fears of spreading the virus among workers looms large, and there are also shortages of components, bringing woes to manufacturing. To top it off, consumer confidence is down. Fewer people buying cars means automakers need to curtail production in response.

Since this is one of the largest steel consuming industries, when automotive production slows, the demand for steel goes down. That in turn places a lot of pressure on the steel industry as a whole. Recovery is likely to depend on how quickly automakers can go back to pre-pandemic production levels. Right now, companies such as Volvo, Toyota and Nissan are implementing plans to begin reopening factories—but consumer demand is still a major issue. During the first quarter of 2020, Fiat Chrysler reported a 10% drop in sales, General Motors saw a 7% drop, Honda a 19% decline, and Hyundai 11%.

What Does This Mean for Steel Markets?

Consumer confidence is likely to remain low through the duration of the pandemic—and that will lead to sluggish auto sales, which will lead to a slump in demand for steel. Other industries, like the non-residential construction sector remain strong, but with steel demands tumbling, we may see shortages along with rising prices.

The question that people in the construction industry may ask themselves: How prevalent will those shortages be, and how high will prices go? That’s the part that is difficult to predict because the pandemic is an ever-evolving situation. Certainly, for anyone who relies on the steel industry, tight times are ahead, and a lot of uncertainty remains.

It’s important to keep in mind that despite the difficulties, this is not an unrecoverable situation, particularly for businesses in the construction sector. With foresight and planning, it’s possible to prevent project delays and bear through COVID-19, especially in the commercial construction industry, which is still moving forward despite these tough times.

We’ve experienced market fluctuations before–particularly during the 2009 financial crisis. Granted, this crisis is unprecedented, and during unprecedented times, the markets also follow suit into the unknown. But even though we are in the midst of a crisis, this will pass just like the hardships we’ve weathered before it.

*Read the Full Report from the Independent Steel Alliance Here.